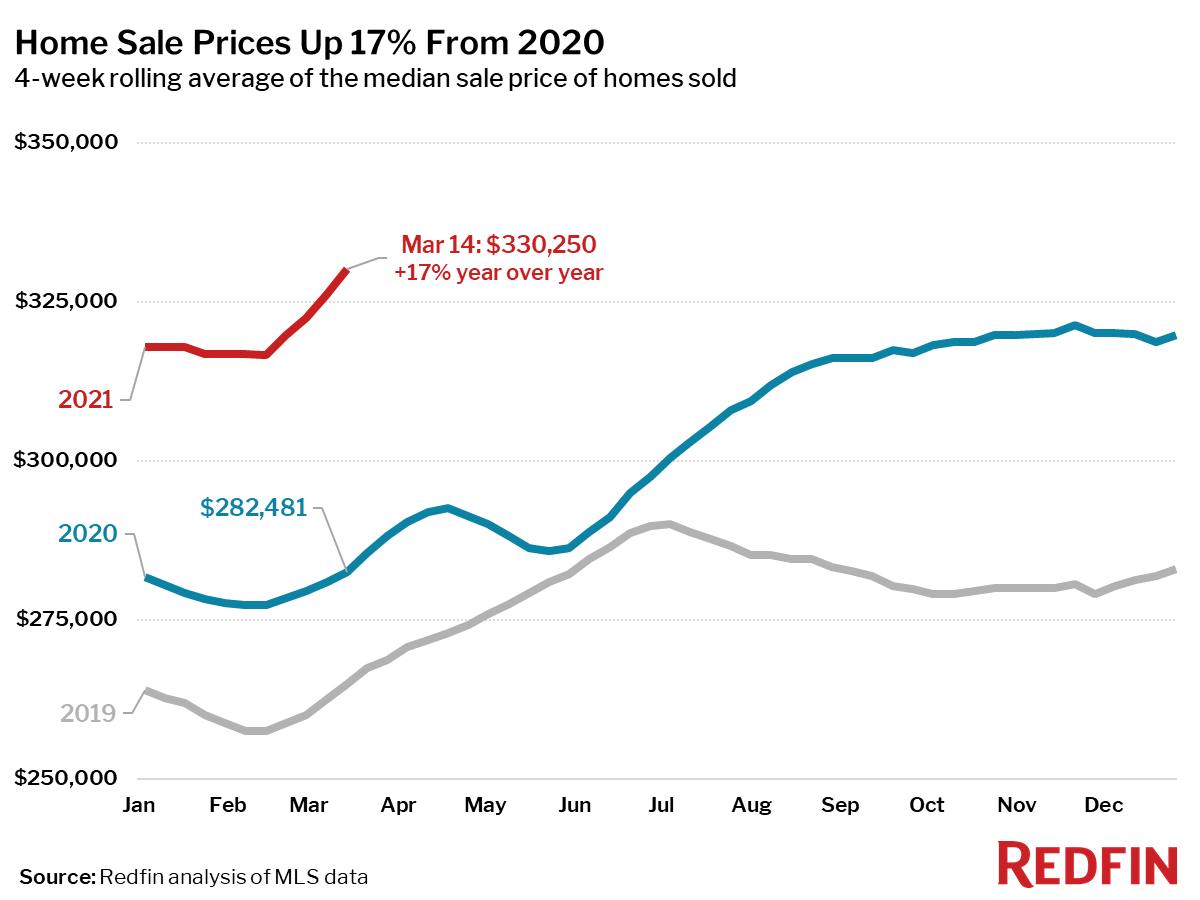

The median home sale price increased 17% year over year to $330,250—an all-time high—according to a new report from Redfin, the technology-powered real estate brokerage. This is the largest increase on record in this data set, which goes back through 2016.

Below are other key housing market takeaways for more than 400 U.S. metro areas during the 4-week period ending March 14.

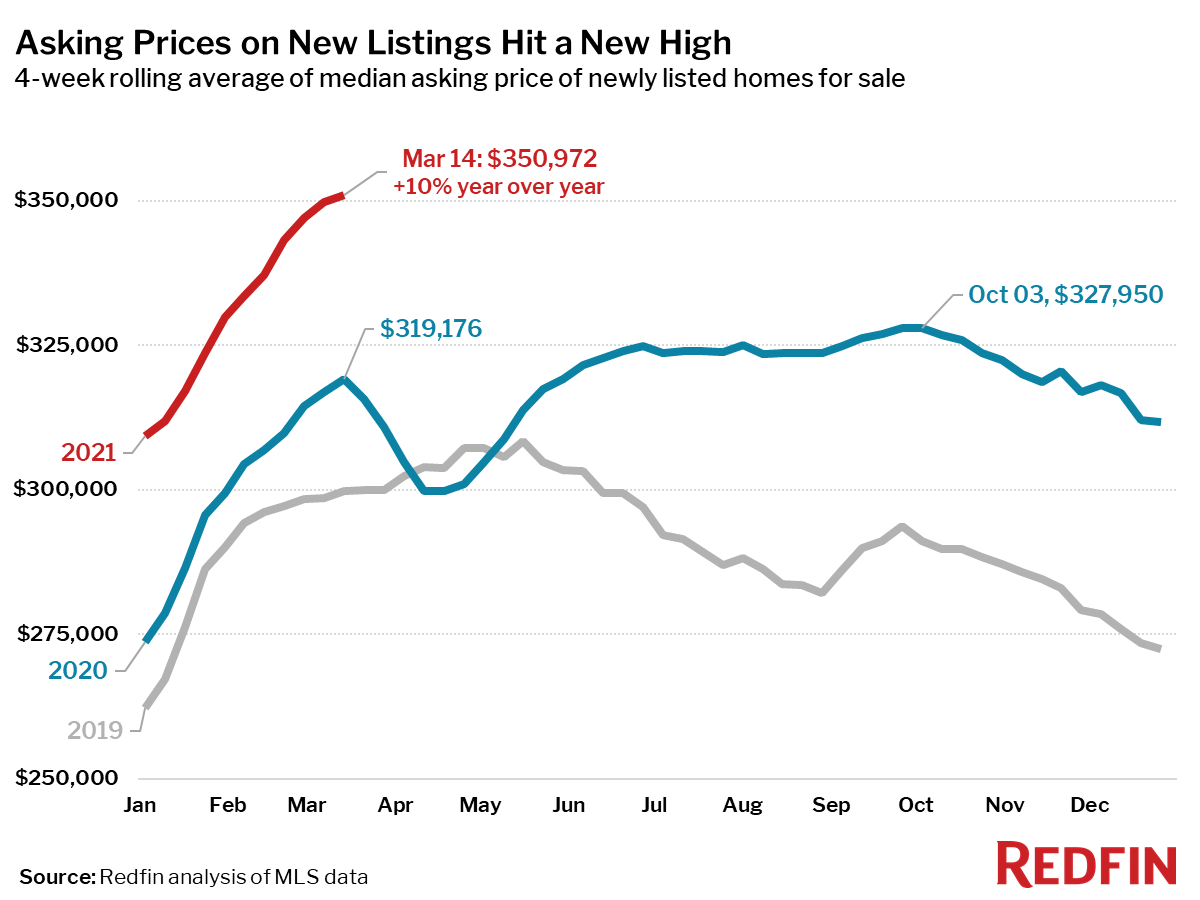

- Asking prices of newly listed homes hit a new all-time high of $350,972, up 10% from the same time a year ago.

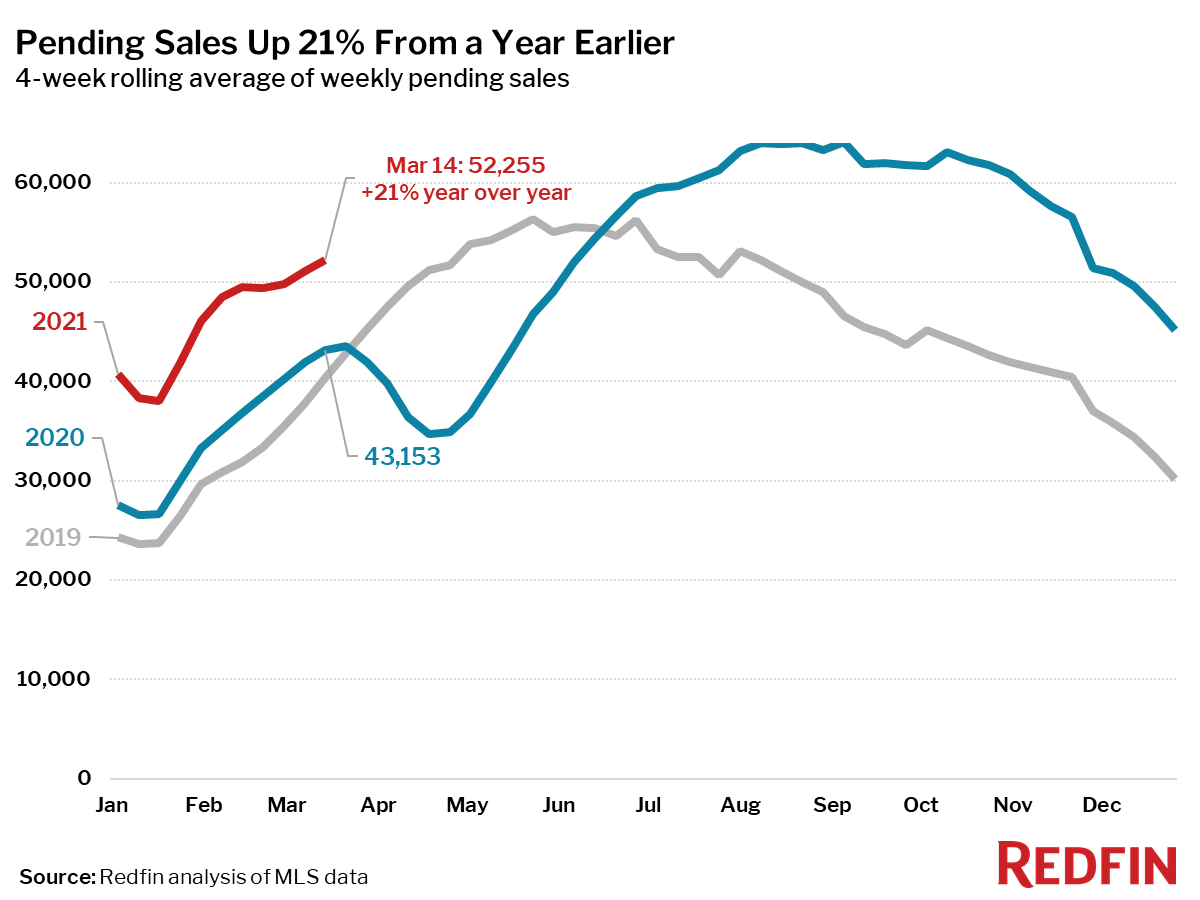

- Pending home sales were up 21% year over year, the smallest increase since August.

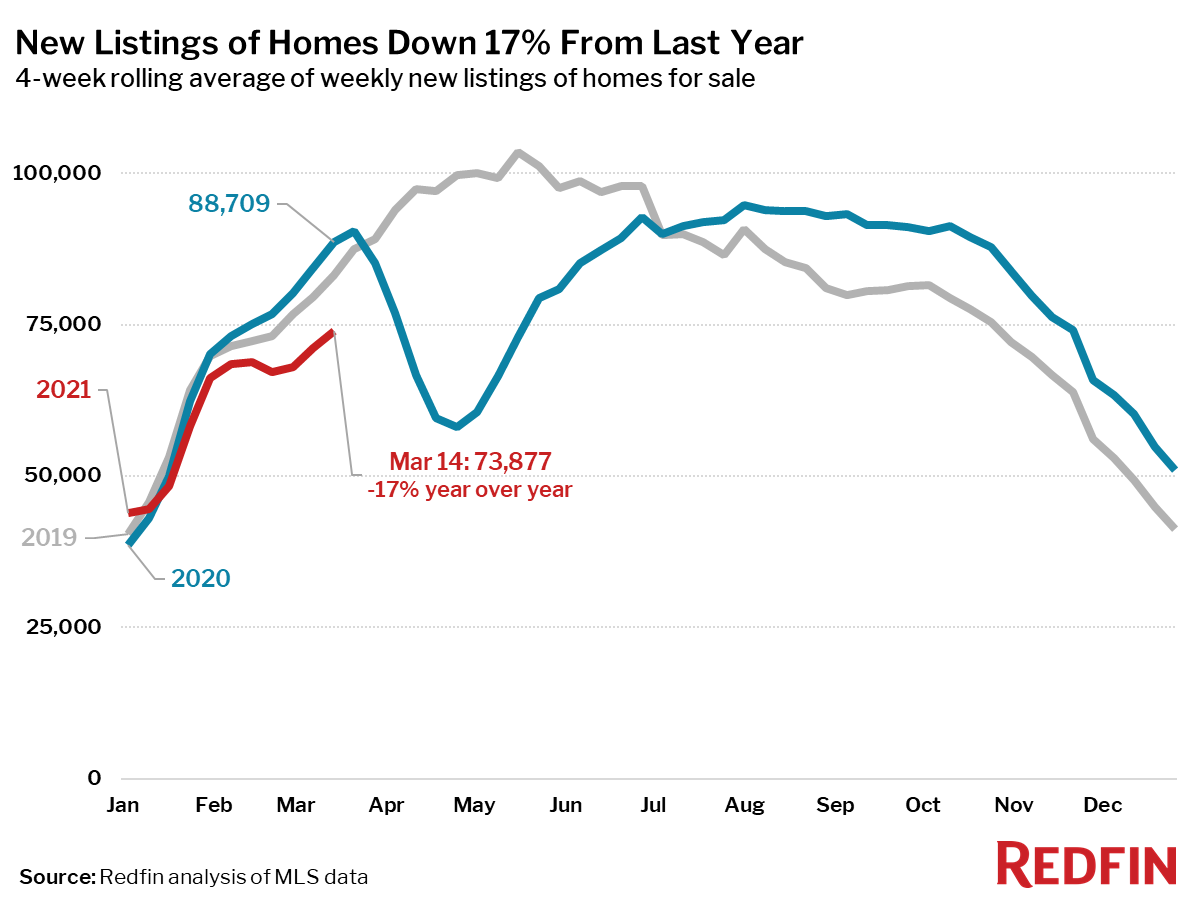

- New listings of homes for sale were down 17% from a year earlier.

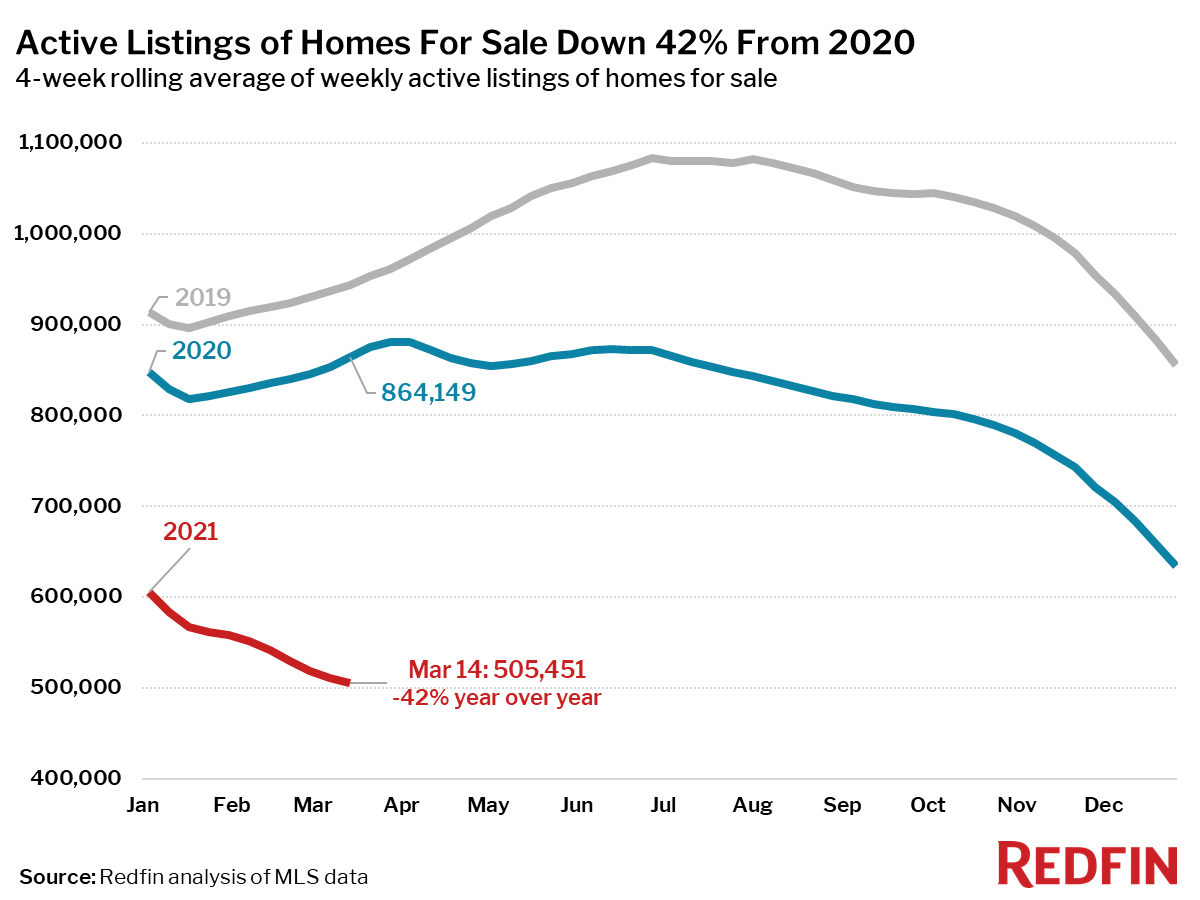

- Active listings (the number of homes listed for sale at any point during the period) fell 42% from 2020 to a new all-time low. This is the largest decrease on record in this data, which goes back through 2016.

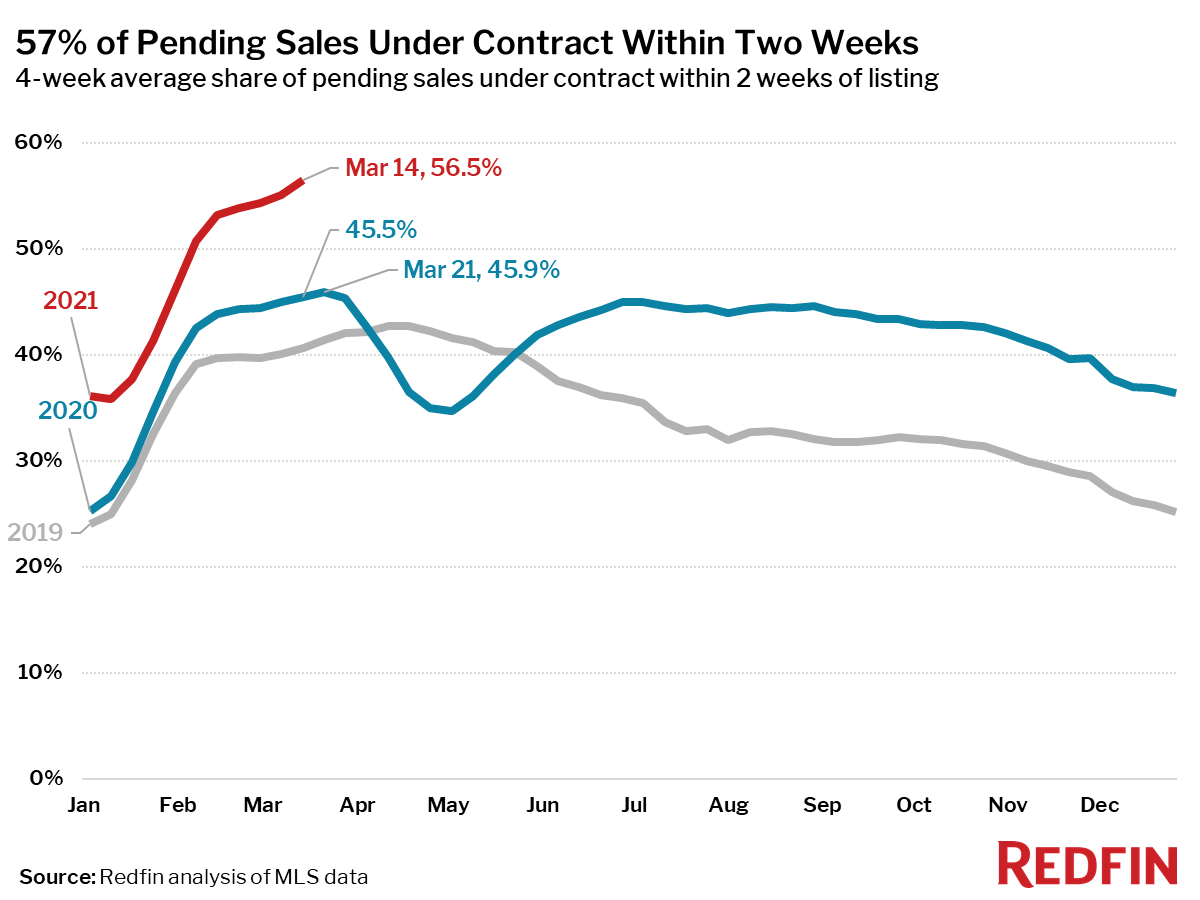

- 57% of homes that went under contract had an accepted offer within the first two weeks on the market, well above the 46% rate during the same period a year ago. This is another new all-time high for this measure since at least 2012 (as far back as Redfin’s data for this measure goes). During the 7-day period ending March 14, 61% of homes sold in two weeks or less.

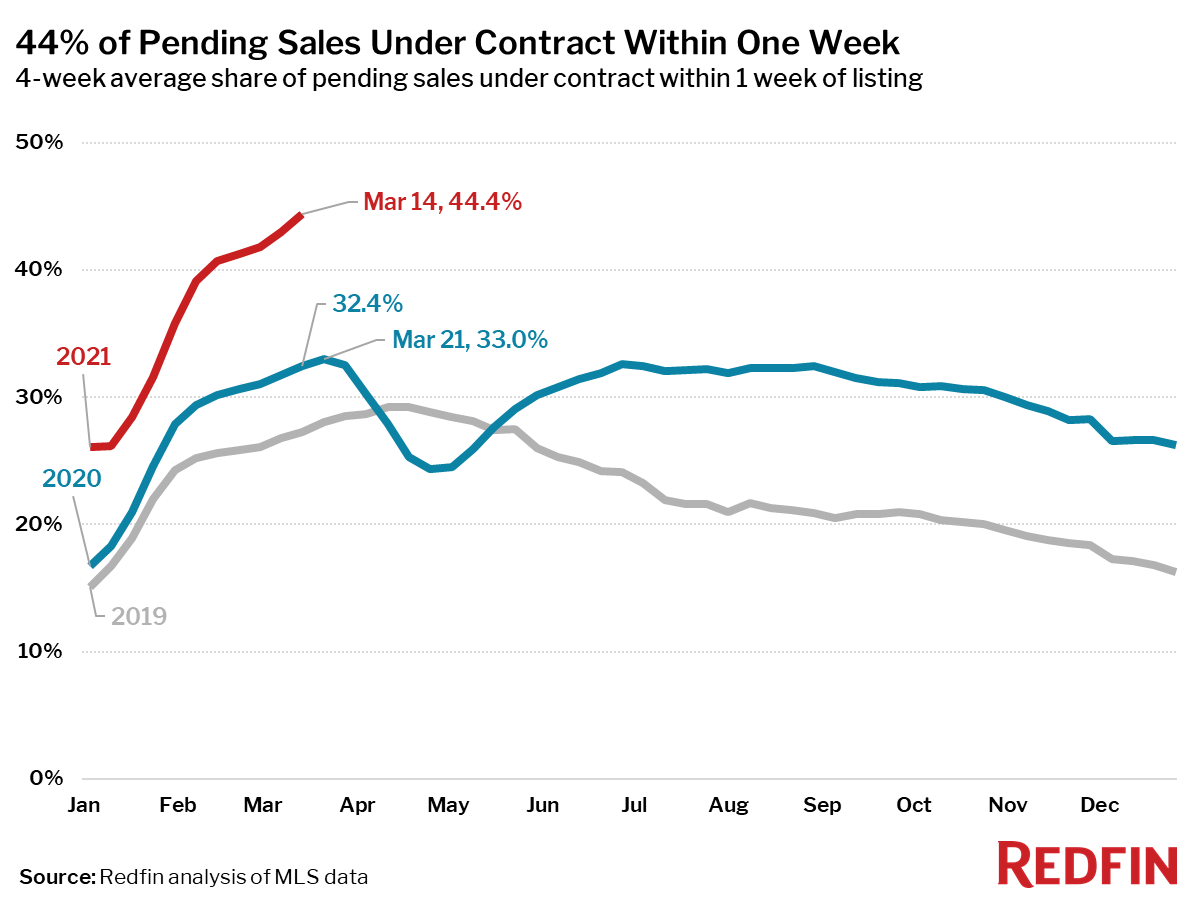

- 44% of homes that went under contract had an accepted offer within one week of hitting the market, up from 32% during the same period a year earlier. This is also an all-time high for this measure. During the 7-day period ending March 14, 48% sold in one week or less.

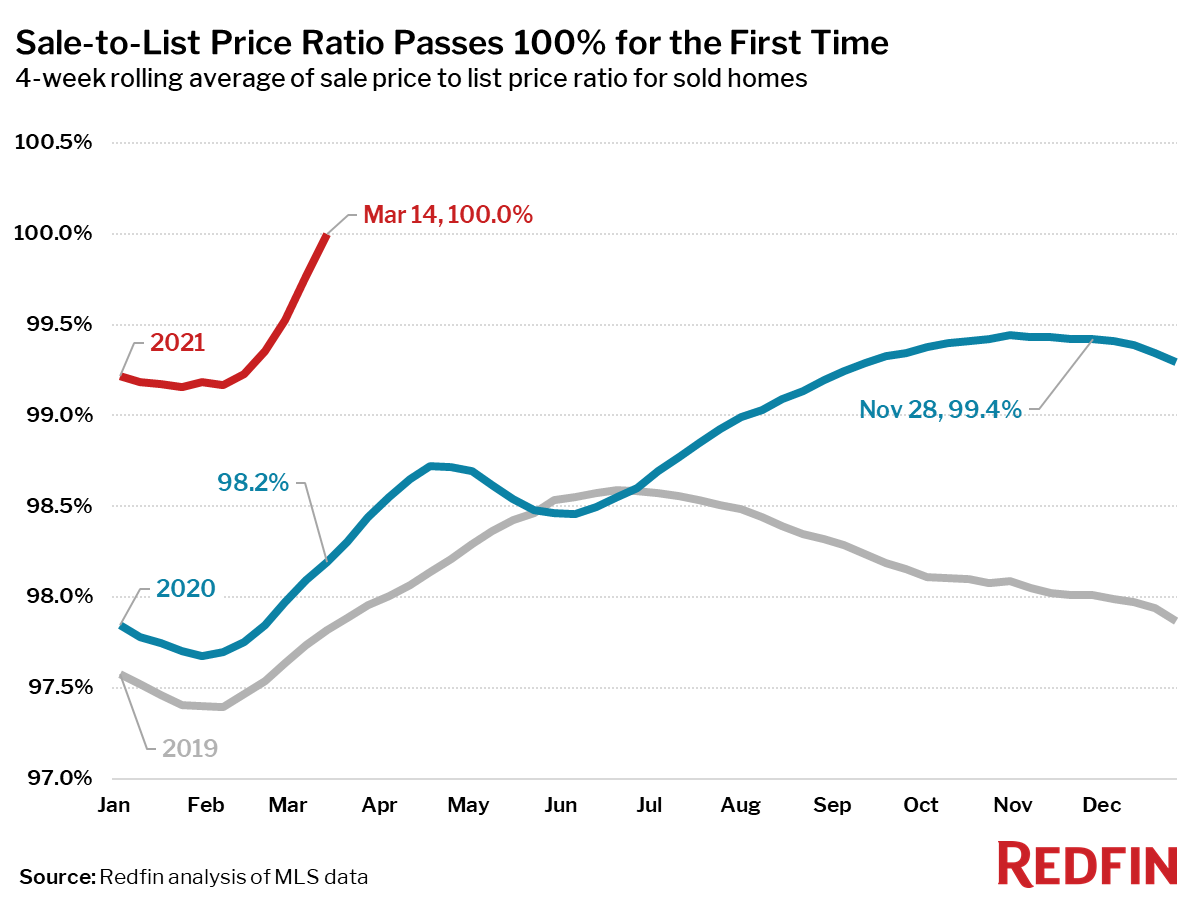

- The average sale-to-list price ratio, which measures how close homes are selling to their asking prices, increased to 100.0%—1.8 percentage points higher than a year earlier, an all-time high and the first time since this data series began in 2016 that the four-week average has exceeded 100% nationwide.

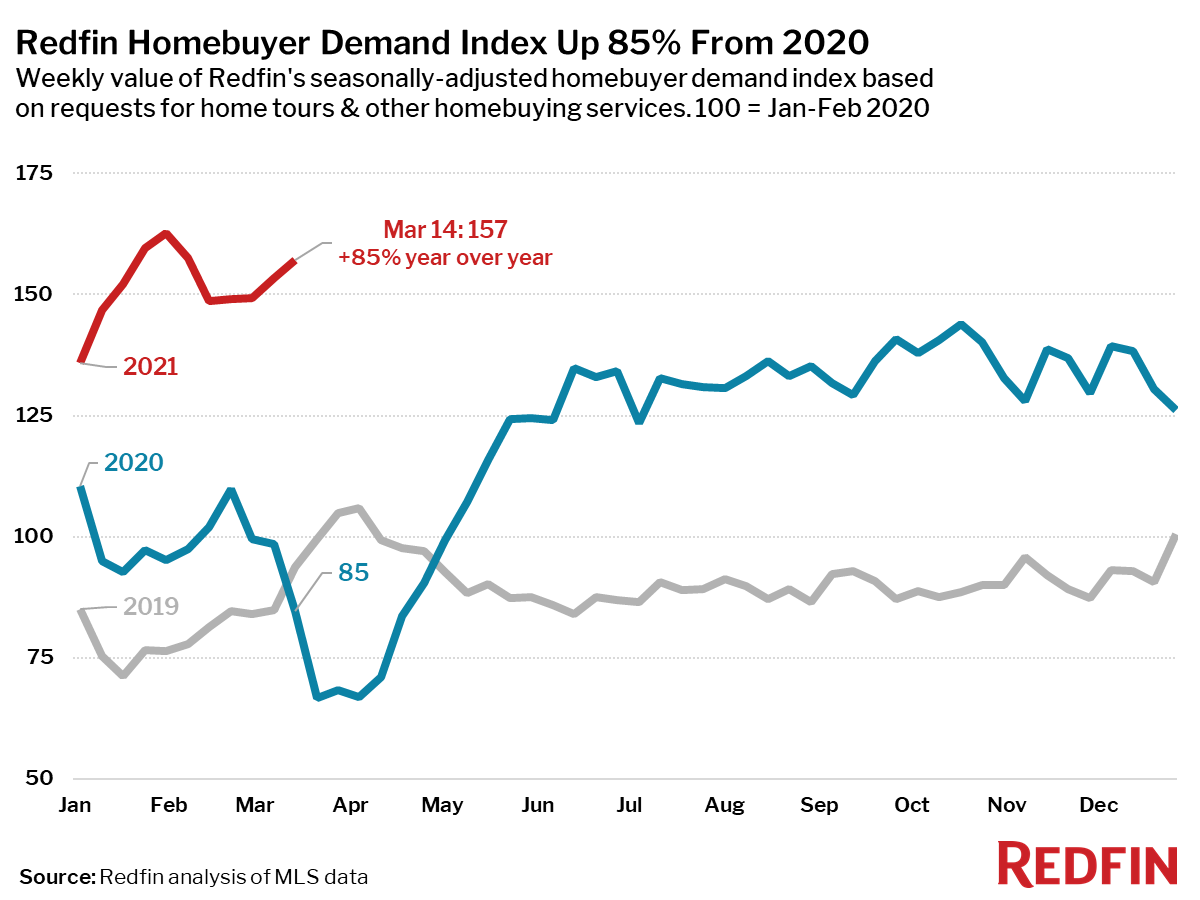

- For the 7-day period ending March 14, the seasonally adjusted Redfin Homebuyer Demand Index—a measure of requests for home tours and other services from Redfin agents—was up 85% from the same period a year ago, when the housing market was dramatically slowing down at the start of the pandemic.

- Mortgage purchase applications increased 2% week over week (seasonally adjusted) and were up 5% from a year earlier (unadjusted) during the week ending March 12. For the week ending March 18, 30-year mortgage rates increased to 3.09%, the highest level since June.

“This time last year, the housing market was shutting down as many cities implemented strict shelter in place orders. A year later the pandemic is still with us, but the housing market is red-hot. It’s so hot some buyers are acting irrationally,” said Redfin Chief Economist Daryl Fairweather. “Some people are willing to do whatever it takes to win a bidding war to the point they may be overpaying. Still, I wouldn’t call this a housing bubble because the demand for homes is truly there and the buyers can afford these high prices. Bubbles burst; I don’t see that happening. The best hope buyers have is that home prices start to grow at a slower pace, but I don’t expect prices to fall.”

In the coming weeks, as the nation’s housing market enters the period where comparisons to a year ago overlap with a steep decline in homebuying demand at the start of the pandemic, many housing demand measures will begin to show very large year-over-year increases. Redfin will provide context around those measures in its reporting as new data becomes available.