Global consumer confidence ticked up to another record high in the second quarter of 2021, according to The Conference Board Global Consumer Confidence Survey, as economic activity improved, mobility restrictions were loosened, vaccines were distributed, and COVID-19 cases declined in many regions. But concerns over health, economic recovery, and job prospects remained for many consumers worldwide amid an uneven reemergence from COVID-19.

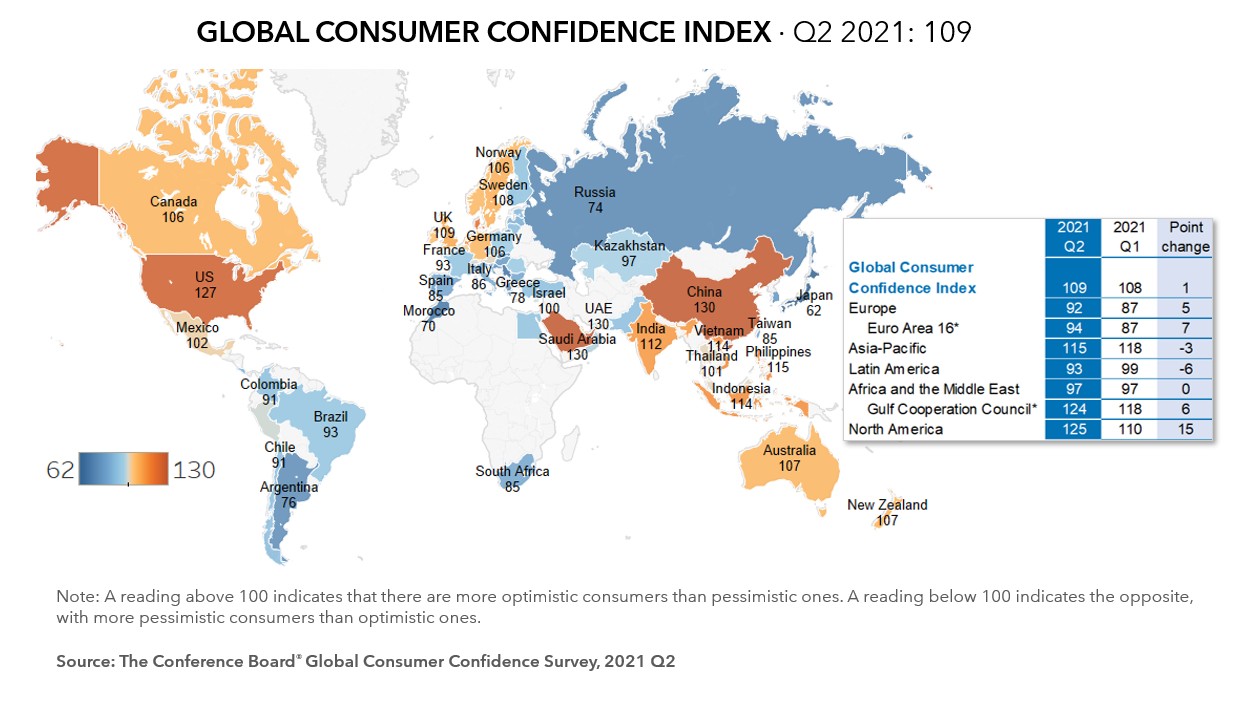

The survey found that overall global consumer confidence rose slightly to 109 in Q2 2021 from 108 in Q1 (a figure above 100 is considered positive.) The global index now surpasses the 106 reading registered at the pandemic’s onset in Q1 2020 and is the highest recorded since the survey began in 2005. Confidence rose in 42 of 65 markets (65%) surveyed, with the strongest gains in regions like North America and Europe with relatively high vaccination rates. On the other hand, confidence declined in regions wrestling with new infections, low vaccine availability, and ongoing economic restrictions.

“Consumer confidence continued to climb worldwide in Q2, albeit at a much slower rate than the 10-pt gain recorded in Q1,” said Dana Peterson, Chief Economist of The Conference Board. “This reflects a global economic recovery that remains highly uneven, with many economies still struggling to contain COVID-19 amid a shortage of vaccines, new variants, and supply-chain bottlenecks that are raising prices. Nonetheless, the elevated level of global consumer confidence bodes well for spending and, consequently, the global economic revival in the second half of this year and into 2022.”

Additional takeaways include:

The record-setting global economic confidence was driven by declining COVID-19 cases, reopening of economies, and loosening of restrictions, but major health and economic woes remain elsewhere:

- Confidence continued to climb from a high base in North America and the Gulf region. North America, where confidence already stood at a strong 110 in Q1, surged further to 125 in Q2—reflecting continued fiscal and monetary support as well as ongoing vaccination campaigns and loosened mobility restrictions. Members of the Gulf Cooperation Council (GCC)—where confidence stands at 124 (+6 pts)—also benefited from fast vaccine rollouts that have enabled a return of tourism.

- Confidence is also returning to Europe. Both the Euro Area 16 (+7 pts to 94) and Europe as a whole (+5 pts to 92) saw confidence climb, led by improving sentiment around financial conditions. Decreasing COVID-19 cases and accelerating vaccination rates across most of Europe contributed to the improved outlook from Q1’s low base.

- Confidence in Asia-Pacific ticked down overall as countries faced diverging COVID situations across the region. While confidence in the Asia-Pacific remained relatively high in Q2 (−3 pts to 115), sharp declines were seen in countries—led by India—that faced unexpectedly severe second (or third) waves of COVID-19. Sentiment in China rose, but other data suggests the level of confidence among Chinese consumers might be overstated given less optimistic reports on employment, retail sales, and household saving.

- Latin America took a step backwards. Confidence across Latin America fell 6 pts in Q2 to 93, with only Peru recording a positive gain. Amid a strong winter surge in COVID-19 cases, heightened political and economic uncertainty in countries like Colombia and Argentina weighed on consumer sentiment in the region.

Overall, the second quarter of 2021 saw the world’s consumers inch back toward more typical pre-pandemic spending patterns:

- Spending intentions drove Q2’s confidence gains. Among the three drivers of overall consumer confidence, spending intensions were solely responsible for the uptick in global sentiment. The proportion of respondents reporting that now was a “good” or “excellent” time to buy needed or wanted goods and services edged up, with the improvement most notable in North America, Asia-Pacific, and Europe. Meanwhile, perceptions of job prospects and personal finances remained relatively unchanged.

- Consumers are planning to spend as economies reopen. A year and a half after the start of the pandemic, the majority (56%) of global consumers were still focused on using spare cash for saving. This was followed more distantly by desires to purchase new clothing (37%) and holidays and vacations (33%). The focus on savings indicates remaining caution among consumers. However, the desire to buy clothing and spend on travel also indicates that consumers are looking forward to reduced mobility and travel restrictions.

- Signs of rising inflation are not hampering spending thus far. Despite rising prices for commodities, food, energy, and a host of goods and select services in reviving economies, only very small percentages of consumers cited inflation as a problem over the next 6 months in areas like food prices (5%), utility bills (2%), or fuel costs (1%). Altogether, just 8% of respondents stated that some form of price increase was their greatest worry—unchanged from Q1 and below the pre-pandemic share of 11%.

Fewer consumers believed their country is in a recession—but concerns over health, the economy, and job security remain elevated.

- A majority (60%) of global consumers still believed their economy was in recession in Q2—down sharply from the peak of 86% reached a year ago. This suggests material improvement in the global economy, again led by rebounds in several major markets, including China, the US, and parts of Emerging Market Asia and Western Europe.

- Health remained the greatest concern among global consumers—edging up to 23% in Q2 from 22% the previous quarter.

The economy (16%) and job security (12%) remain high-priority issues. But concerns in these areas have ticked down compared to Q1 and are down sharply from a year ago.