After a remarkably hot summer, home sales are expected to peak this fall then taper off in 2021 while staying above pre-pandemic levels, according to a forecast by Zillow’s team of economists in this week’s Market Report. Key market stats from the week ending Sept. 19 show depleted inventory levels plumbing new depths and prices skyrocketing over 2019 figures.

FORECAST: Housing market outlook improves, with major unknowns tempering expectations

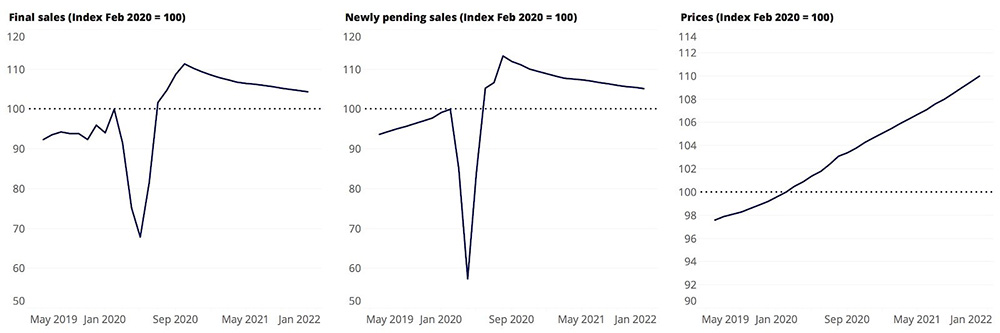

Sales expected to stay high but taper down through 2021. Zillow’s team of economists expect seasonally adjusted home sales to peak this fall then gradually decline through 2021. Sales volumes overall are forecasted to remain higher than pre-pandemic levels throughout this year and next.

Home price outlook adjusted higher for coming year. Seasonally adjusted home prices are expected to increase 1.2% from August to November and rise 4.8% between August 2020 and August 2021. Zillow Research’s previous forecast predicted a 3.8% increase in home prices over this time frame.

Here’s why: Zillow’s predictions for seasonally adjusted home prices and pending sales are more optimistic than previous forecasts because sales and prices have stayed strong through the summer months amid increasingly short inventory and high demand. The pandemic also pushed the buying season further back in the year, adding to recent sales. Future sources of uncertainty including lapsed fiscal relief, the long-term fate of policies supporting the rental and mortgage market, and virus-specific factors, were incorporated into this outlook.

KEY STATS: Market update for the week ending Sept. 19

Rate of homes going under contract slows slightly, but time on market still short

- Buyers are still extremely keen to purchase houses, with newly pending sales up 21.8% compared to last year. However, the frenzied activity of the summer is showing signs of the typical fall slowdown, dropping 2.8% compared to a month ago and down 1% since the week prior.

- Typical time-on-market for listings stayed steady at 13 days, which is 14 days quicker than last year. Among the 50 largest U.S. markets, Cincinnati and Columbus, Ohio, shared the shortest typical time on market at four days to pending. Nashville posted the longest typical time on market at 33 days, while New York and Virginia Beach both marked 32.

Inventory shortage falls further

- Total inventory dropped even further in a steady decline that began the first week of June. For-sale listings fell an enormous 34.6% below this week last year; the largest year-over-year deficit seen since Zillow’s weekly stats began in 2019.

- There were 13.6% fewer new listings last week than at this point last year.

Prices soar amid strong demand and low supply

- The median sale price continued its meteoric rise to $284,000 as of the week ending Aug. 8, 8.7% higher than the previous year and the largest year-over-year increase seen since at least the beginning of 2019. Sale prices were up 2% over the month prior.

- The median list price rose to $345,000, a full 10% over last year but just 0.1% higher than a month prior.

New home sales astound in August

- New home sales have been particularly robust, even within this astounding buying season. The annualized pace of new home sales in August exceeded 1 million homes — a benchmark unseen since 2006.

|

Metropolitan Area* |

Newly |

Newly |

Median |

Total |

New |

New |

Median |

Median |

|

United States |

21.8% |

-1.0% |

13 |

-34.6% |

-13.6% |

4.2% |

284000 |

8.7% |

|

New York/Newark, NY/NJ |

60.4% |

0.8% |

32 |

-20.1% |

-11.5% |

-0.8% |

445000 |

2.7% |

|

Los Angeles, CA |

8.1% |

0.7% |

12 |

-24.9% |

8.4% |

3.4% |

713375 |

7.7% |

|

Chicago, IL |

38.2% |

-2.2% |

13 |

-28.5% |

-1.0% |

8.7% |

264500 |

7.3% |

|

Dallas-Fort Worth, TX |

30.6% |

-0.3% |

23 |

-31.8% |

-24.4% |

1.4% |

303812 |

9.1% |

|

Philadelphia, PA |

37.1% |

3.3% |

9 |

-37.3% |

-5.8% |

10.5% |

279000 |

5.3% |

|

Houston, TX |

25.4% |

-0.2% |

17 |

-29.1% |

-17.3% |

8.2% |

271529 |

9.9% |

|

Washington, DC |

21.8% |

2.9% |

7 |

-34.4% |

-1.6% |

3.6% |

459431 |

8.4% |

|

Miami-Fort Lauderdale, FL |

40.1% |

2.6% |

27 |

-13.4% |

-12.3% |

4.6% |

329750 |

12.4% |

|

Atlanta, GA |

15.8% |

-3.3% |

14 |

-30.6% |

-22.0% |

6.3% |

283850 |

10.4% |

|

Boston, MA |

6.3% |

2.4% |

8 |

-30.5% |

-18.9% |

1.6% |

522500 |

8.1% |

|

San Francisco, CA |

34.4% |

-1.6% |

12 |

-4.3% |

3.1% |

24.0% |

896500 |

12.1% |

|

Detroit, MI |

41.8% |

-3.3% |

8 |

-38.1% |

-14.9% |

12.1% |

222975 |

11.7% |

|

Riverside, CA |

12.0% |

-1.4% |

9 |

-48.1% |

6.6% |

6.0% |

411250 |

10.3% |

|

Phoenix, AZ |

18.9% |

3.1% |

11 |

-21.6% |

0.0% |

11.9% |

322500 |

11.9% |

|

Seattle, WA |

20.5% |

-2.3% |

6 |

-32.2% |

-6.3% |

-2.8% |

535525 |

11.1% |

|

Minneapolis-St. Paul, MN |

31.2% |

1.1% |

17 |

-27.1% |

3.9% |

-0.3% |

311625 |

9.3% |

|

San Diego, CA |

8 |

-38.2% |

2.5% |

-1.7% |

635188 |

8.9% |

||

|

St. Louis, MO |

16.8% |

-1.6% |

6 |

-38.4% |

-11.2% |

14.7% |

217912 |

10.7% |

|

Tampa, FL |

8 |

-34.8% |

-16.4% |

-4.4% |

258409 |

9.5% |

||

|

Baltimore, MD |

17.2% |

6.6% |

12 |

-44.8% |

-12.7% |

9.3% |

317500 |

0.8% |

|

Denver, CO |

25.8% |

-1.5% |

6 |

-34.2% |

16.2% |

21.8% |

462881 |

6.5% |

|

Pittsburgh, PA |

52.3% |

1.3% |

9 |

-27.2% |

-2.3% |

11.8% |

199499 |

7.7% |

|

Portland, OR |

21.9% |

-5.5% |

6 |

-37.0% |

-28.4% |

-1.3% |

440225 |

8.6% |

|

Charlotte, NC |

-1.8% |

-1.1% |

6 |

-42.9% |

-19.2% |

14.2% |

286500 |

8.5% |

|

Sacramento, CA |

18.3% |

-1.5% |

7 |

-44.1% |

0.3% |

1.6% |

452875 |

8.1% |

|

San Antonio, TX |

34.4% |

0.6% |

27 |

-25.7% |

-23.1% |

11.0% |

252812 |

8.2% |

|

Orlando, FL |

12 |

-17.0% |

-3.0% |

11.4% |

282562 |

7.8% |

||

|

Cincinnati, OH |

12.0% |

0.7% |

4 |

-39.1% |

-3.7% |

21.9% |

212125 |

11.8% |

|

Cleveland, OH |

70.9% |

0.3% |

18 |

-39.8% |

-0.8% |

-2.5% |

175350 |

9.6% |

|

Kansas City, MO |

15.4% |

-0.6% |

5 |

-43.7% |

-4.9% |

22.8% |

259250 |

12.7% |

|

Las Vegas, NV |

18.5% |

-1.4% |

15 |

-23.3% |

8.3% |

2.3% |

304750 |

-0.1% |

|

Columbus, OH |

18.6% |

0.6% |

4 |

-40.1% |

-11.4% |

10.4% |

240500 |

16.1% |

|

Indianapolis, IN |

14.0% |

2.4% |

5 |

-41.0% |

6.7% |

31.9% |

222625 |

8.4% |

|

San Jose, CA |

-9.7% |

-3.5% |

15 |

-20.2% |

20.3% |

18.1% |

1139375 |

8.6% |

|

Austin, TX |

29.2% |

2.0% |

8 |

-37.0% |

-2.9% |

41.5% |

357978 |

12.4% |

|

Virginia Beach, VA |

32 |

-40.7% |

-1.3% |

0.7% |

276912 |

8.1% |

||

|

Nashville, TN |

33 |

-24.0% |

-36.9% |

17.5% |

317850 |

5.1% |

||

|

Providence, RI |

-2.9% |

3.7% |

13 |

-38.3% |

-24.4% |

4.2% |

318600 |

5.4% |

|

Milwaukee, WI |

28 |

-6.5% |

-6.2% |

31.2% |

207475 |

6.9% |

||

|

Jacksonville, FL |

43.2% |

1.4% |

14 |

-36.7% |

-17.0% |

0.2% |

268362 |

1.3% |

|

Memphis, TN |

33.9% |

1.1% |

7 |

-45.4% |

-20.2% |

6.1% |

209212 |

7.0% |

|

Oklahoma City, OK |

20.4% |

-4.6% |

10 |

-35.5% |

-6.2% |

24.8% |

205750 |

12.5% |

|

Louisville, KY |

3.0% |

-0.6% |

5 |

-43.9% |

-8.3% |

1.3% |

217812 |

9.0% |

|

Hartford, CT |

49.6% |

-1.3% |

10 |

-41.5% |

5.7% |

10.9% |

258800 |

7.8% |

|

Richmond, VA |

6 |

-39.9% |

-10.0% |

9.3% |

284688 |

7.9% |

||

|

New Orleans, LA |

4.1% |

-1.7% |

17 |

-44.0% |

-20.8% |

-2.0% |

232875 |

6.6% |

|

Buffalo, NY |

18.7% |

-2.5% |

10 |

-36.2% |

-8.6% |

-0.3% |

189850 |

9.7% |

|

Raleigh, NC |

15.0% |

1.3% |

5 |

-41.4% |

-25.7% |

13.1% |

312812 |

5.8% |

|

Birmingham, AL |

43.2% |

0.9% |

8 |

-35.4% |

9.3% |

22.3% |

224942 |

4.8% |

|

Salt Lake City, UT |

6 |

-45.5% |

-33.7% |

29.8% |

381916 |

11.2% |

|

*Table ordered by market size |

|

**Sale price data as of the week ending Aug. 8 |